I. Introduction

In May 2026, KHL Group’s International Construction magazine released the latest edition of the “Yellow Table” – the annual ranking of the world’s top construction equipment companies. As a widely recognized authority in the sector, this year’s report signals several key trends: global total revenue has reached a historic high of $246.5 billion, the top ten rankings have seen significant reshuffling, and Chinese manufacturers have collectively risen to reshape the regional competitive landscape.

This article, based on official KHL data, examines the industry logic and future trends behind the 2026 Yellow Table.

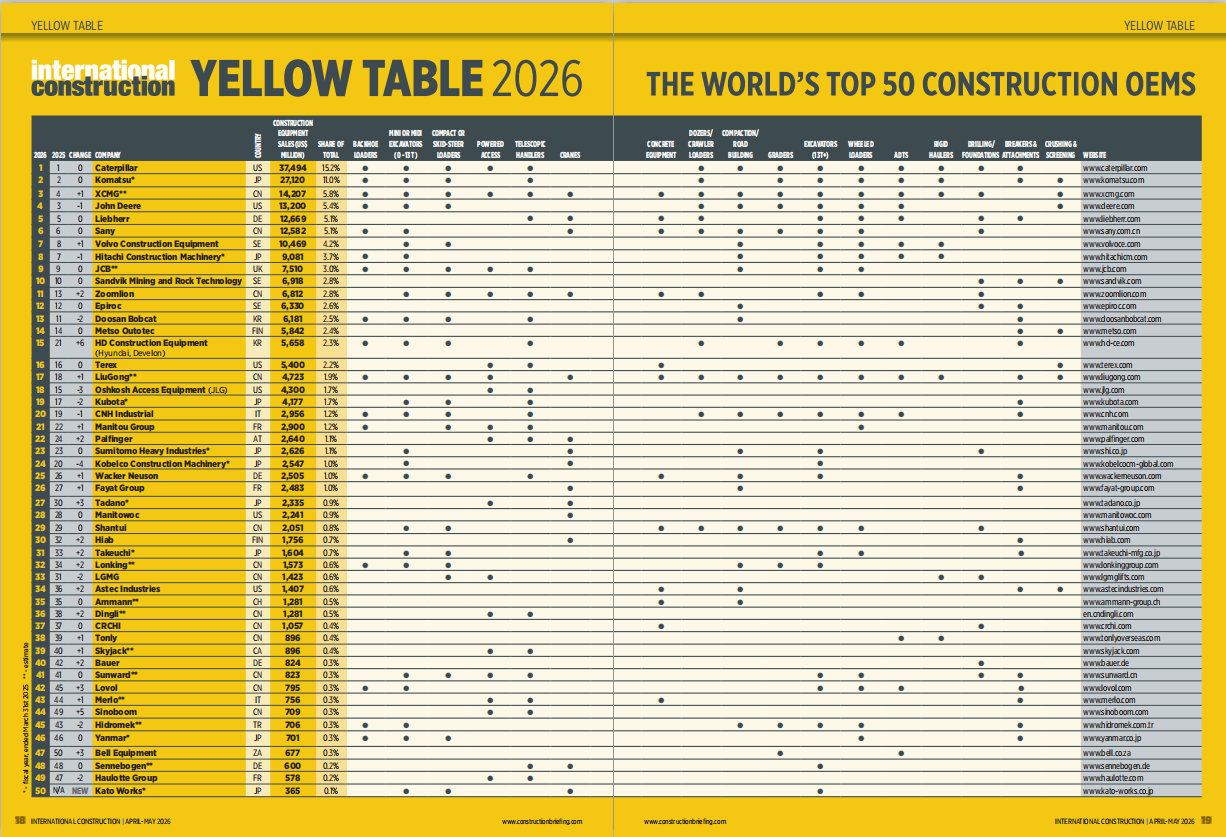

| Rank | Change | Company Name | Country | Revenue ($B) | Market Share |

| 1 | – | Caterpillar | US | 374.94 | 15.70% |

| 2 | – | Komatsu | JP | 271.2 | 11.00% |

| 3 | ↑1 | XCMG | CN | 142.07 | 5.80% |

| 4 | ↓1 | John Deere | US | 132 | 5.40% |

| 5 | – | Liebherr | DE | 126.69 | 5.70% |

| 6 | – | Sany | CN | 125.82 | 5.70% |

| 7 | ↑1 | Volvo CE | SE | 104.69 | 4.20% |

| 8 | ↓1 | Hitachi | JP | 90.81 | 3.70% |

| 9 | – | JCB | GB | 75.1 | 3.00% |

| 10 | – | Sandvik | SE | 69.18 | 2.80% |

| 11 | ↑2 | Zoomlion | CN | 68.12 | 2.80% |

| 12 | – | Epiroc | SE | 63.3 | 2.60% |

| 13 | ↓2 | Doosan Bobcat | KR | 61.81 | 2.50% |

| 14 | – | Metso Outotec | FI | 58.42 | 2.40% |

| 15 | ↑6 | HD Hyundai | KR | 56.58 | 2.30% |

| 16 | – | Terex | US | 54 | 2.20% |

| 17 | ↑1 | Liugong | CN | 47.23 | 1.90% |

| 18 | ↓3 | JLG | US | 43 | 1.70% |

| 19 | ↓2 | Kubota | JP | 41.77 | 1.70% |

| 20 | ↓1 | CNH Industrial | IT | 29.56 | 1.20% |

| 21 | ↑1 | Manitou | FR | 29 | 1.20% |

| 22 | ↑2 | Palfinger | AT | 26.4 | 1.10% |

| 23 | – | Sumitomo | JP | 26.26 | 1.10% |

| 24 | ↓4 | Kobelco | JP | 25.47 | 1.00% |

| 25 | ↑1 | Wacker Neuson | DE | 25.05 | 1.00% |

| 26 | ↑1 | Fayat Group | FR | 24.83 | 1.00% |

| 27 | ↑3 | Tadano | JP | 23.35 | 0.90% |

| 28 | – | Manitowoc | US | 22.41 | 0.90% |

| 29 | – | Shantui | CN | 19.81 | 0.80% |

| 30 | ↑2 | Hiab | FI | 17.56 | 0.70% |

| 31 | ↑2 | Takeuchi | JP | 16.04 | 0.70% |

| 32 | ↑2 | Longking | CN | 15.73 | 0.60% |

| 33 | ↑2 | Lingong | CN | 14.23 | 0.60% |

| 34 | ↑2 | Astec Industries | US | 14.07 | 0.60% |

| 35 | – | Ammann Group | CH | 12.81 | 0.50% |

| 36 | ↑2 | Dingli | CN | 12.81 | 0.50% |

| 37 | – | CRCHI | CN | 10.57 | 0.40% |

| 38 | ↑1 | Tonly | CN | 8.96 | 0.40% |

| 39 | ↑1 | Skyjack | CA | 8.96 | 0.40% |

| 40 | ↑2 | Bauer | DE | 7.57 | 0.30% |

| 41 | – | Sunward | CN | 8.23 | 0.30% |

| 42 | ↑3 | Lovol | CN | 7.95 | 0.30% |

| 43 | ↑1 | Halo Group | IT | 7.56 | 0.30% |

| 44 | ↑5 | Sinoboom | CN | 7.09 | 0.30% |

| 45 | ↓2 | Hidromek | TR | 7.06 | 0.30% |

| 46 | – | Yanmar | JP | 7.01 | 0.30% |

| 47 | ↑3 | Bell Equipment | ZA | 6.77 | 0.30% |

| 48 | – | Sennebogen | DE | 6 | 0.20% |

| 49 | ↓2 | Haulotte | FR | 5.78 | 0.20% |

| 50 | NEW | Kato | JP | 3.65 | 0.10% |

II. Market Peak of Top Construction Equipment Companies

1. Total Revenue Reaches New High

Total revenue of the 50 largest firms: $246.528 billion, a 3.8% increase year-on-year.

This marks the third time in five years that the total has reached an all-time high, indicating that the global construction machinery industry is in a confirmed recovery phase.

2. Divergent Regional Growth

According to analysis by Off-Highway Research:

Growth markets: China and most emerging economies.

Stable/soft markets: Europe remained flat; North America saw a slight decline.

The global growth engine is shifting from traditional European and North American markets toward China and other emerging regions.

III. Big Three Shift in Heavy Construction Equipment Manufacturers

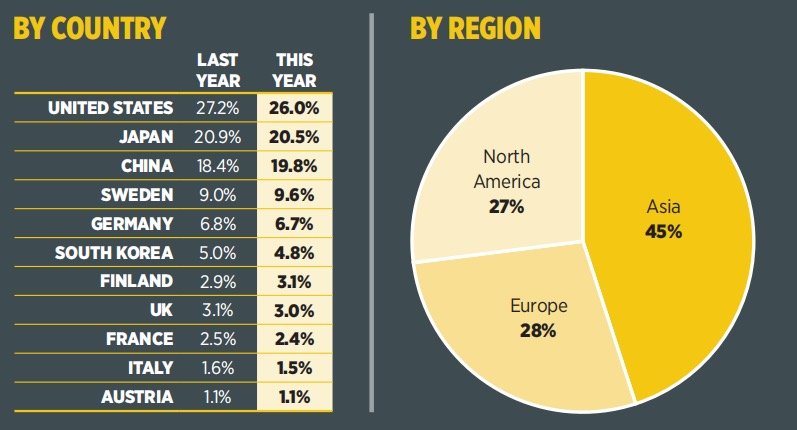

The United States, Japan, and China together account for more than 66% of total revenue among the top 50, but their shares are diverging:

| Country | Key Trend |

|---|---|

| United States | Slightly declining revenue share |

| Japan | Slightly declining revenue share |

| China | Rising market share |

Regional revenue share:

Asian manufacturers: 45% (slightly up)

European manufacturers: 28% (marginally up)

North American manufacturers: 27% (slightly down)

The center of gravity in the global heavy construction equipment manufacturers landscape is shifting persistently toward Asia, and China in particular.

IV. Top 10 Construction Equipment Manufacturers in World

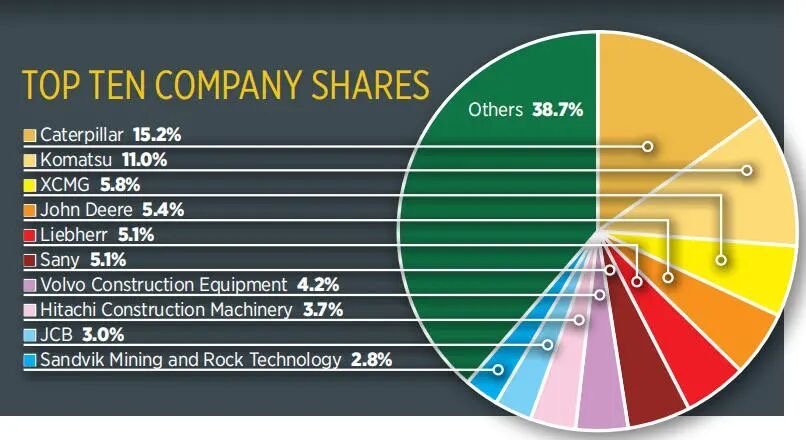

The most dramatic development in this year’s ranking is the upheaval within the top ten.

1. The Undisputed Leaders

Caterpillar and Komatsu remain firmly in first and second place.

2. Historic Breakthrough at No. 3: XCMG

This is the highest ranking ever achieved by a Chinese construction equipment brand in the Yellow Table. The KHL report specifically notes that this results from leading Chinese firms like XCMG focusing increasingly on international markets – many now generate more than half of their revenue overseas.

3. Other Changes

John Deere fell to fourth place.

Volvo CE and Hitachi Construction Machinery swapped positions, taking seventh and eighth respectively.

Liebherr (fifth), Sany (sixth), JCB (ninth), and Sandvik (tenth) remained unchanged.

V. China’s Rise in Construction Machinery Industry

The performance of Chinese manufacturers is the brightest segment of this year’s report. Within the global construction machinery industry, China’s ascent is unmistakable.

1. Core Data

Number of listed companies: 13

Total revenue: $48.862 billion

Global market share: 20.4%

2. Rising Rankings and Industrial Cluster Effect

Unlike previous years when many Chinese firms appeared but ranked lower, this year there has been a general upward movement in their positions. From an industrial agglomeration perspective, among the 13 listed Chinese firms: five from Hunan Province contributed 45% of China’s total revenue and 9.5% of the global total; one from Jiangsu Province (XCMG) accounted for 29.1% of China’s revenue; and three from Shandong Province were on the list.

VI. Top Chinese Construction Equipment Manufacturers: Brand Profiles

Top Chinese construction equipment manufacturers have built diverse competitive advantages across multiple segments. Below are detailed profiles of the 13 Chinese firms on the 2026 Yellow Table.

1. XCMG – No. 3

Founded: Predecessor Huaxing Iron Works established in 1943; group formally founded in 1989

Main Products: Lifting machinery, mining machinery, excavators, concrete machinery, piling machinery, road machinery, aerial work platforms, environmental sanitation machinery, agricultural machinery, emergency rescue equipment

Core Strengths: Lifting machinery ranks first globally; created over 100 domestic first-of-its-kind products; products exported to over 190 countries

2. Sany Heavy Industry – No. 6

Founded: 1994

Main Products: Excavators, concrete machinery, cranes, piling machinery, road machinery

Core Strengths: Excavators ranked first globally by cumulative sales over past five years; overseas revenue accounts for 57.4%; products sold to over 150 countries

3. Zoomlion – No. 11

Founded: 1992

Main Products: Concrete machinery, cranes, aerial work platforms – 15 categories, 75 product series

Core Strengths: Holds five national manufacturing champion products; led development of over 30 international standards (most in industry); overseas revenue exceeds 54%

4. Liugong – No. 17

Founded: 1958

Main Products: Earthmoving machinery, mining machinery, cranes, industrial vehicles, agricultural machinery – over 30 product lines

Core Strengths: Developed China’s first wheel loader in 1966; single model ZL50C loader sold over 150,000 units globally; first in industry to go public in 1993

5. Shantui – No. 29

Founded: Predecessor Yantai Machinery Plant established 1952; company formally founded 1993

Main Products: Bulldozers, road machinery, concrete machinery, loaders, excavators, and core components

Core Strengths: Bulldozer production and sales continuously leading globally; ranked first in China for 18 consecutive years; launched world’s first 5G remote-controlled high-horsepower bulldozer

6. Longking – No. 32

Founded: 1993

Main Products: Loaders, excavators, forklifts, rollers, skid-steer loaders – four major categories

Core Strengths: First in industry to list on Hong Kong Stock Exchange in 2005; loader production and sales rank among global leaders; jointly launched next-generation electric loaders with CATL

7. Sunward – No. 36

Founded: 1999

Main Products: Engineering equipment (rotary drilling rigs, excavators), special equipment, aviation equipment

Core Strengths: Leading domestic manufacturer of underground engineering equipment; selected as national manufacturing champion enterprise in 2024; launched China’s first unmanned emergency rescue equipment suite

8. CRCHI – No. 40

Founded: 2007

Main Products: Tunnel boring machines (shield machines/TBMs), rail transit equipment, special equipment

Core Strengths: Achieved domestic production of TBM main bearings (global largest diameter 8.61m); listed on STAR Market in 2021, first spin-off listing from a central SOE

9. Dingli – No. 43

Founded: 2005

Main Products: Various intelligent aerial work platforms (boom lifts, scissor lifts – over 200 models)

Core Strengths: National manufacturing champion enterprise; won IPAF Pioneer Award (first Chinese manufacturer); full product line fully electrified

10. Sinoboom – No. 48

Founded: 2008

Main Products: Straight boom, articulated boom, scissor, spider aerial work platforms

Core Strengths: Leading overseas footprint with manufacturing bases in Poland and Mexico; international revenue approaches 50%; over 90% of European market products are electric drive

11. Lovol – No. 42

Founded: 1998

Main Products: Loaders, excavators, off-road wide-body dump trucks, agricultural equipment

Core Strengths: Developed China’s first multi-stage power hydraulic control system with over 15% energy savings; leverages Weichai Group engine and hydraulic powertrain resources

12. XGMA – Ranked 45-50 range

Founded: 1951

Main Products: Loaders, excavators, forklifts, road machinery, tunnel boring machinery

Core Strengths: Developed China’s first wheel loader in 1964; served as designated brand for China’s Antarctic expeditions for 30 consecutive years since 1992

13. NHL – Ranked 45-50 range

Founded: 1988

Main Products: Off-highway mining trucks (25-400 ton full range) and components

Core Strengths: Over 80% market share in domestic mining trucks; sales ranked first in China, third globally; autonomous driving mining truck fleet ranked third globally

VII. Value Option: Qhmach

Qhmach, founded in 2003, specializes in compaction equipment with a sales network across over 60 countries and annual exports exceeding 500 units. The company also produces excavators and loaders.

Core Strengths:

WD137HF fully hydraulic double-drum vibratory roller won 2019 TOP50 Gold Award

“Hydraulic performance at mechanical prices” strategy

Products sold to over 60 countries in Africa, South America, and Europe

30+ models across four series of rollers

For small and medium-sized contractors, Qhmach offers a focused approach: niche specialization, technological breakthroughs, and lower operating costs.

VIII. Top Chinese Construction Equipment Manufacturers Outlook

Top Chinese construction equipment manufacturers have become a major global force with 13 firms holding 20.4% market share. Looking ahead, they must advance technological innovation, overseas expansion, and brand building.

Their continued rise depends on three factors: maintaining overseas growth amid market volatility, breaking through on high-end components and brand premium, and achieving differentiation among the 13 listed firms.

IX. Conclusion

The 2026 Yellow Table shows that the global construction machinery industry continues to evolve. Top Chinese construction equipment manufacturers have become an important growth force, with 13 firms on the list holding 20.4% of global market share. XCMG entered the global top three for the first time, while Sany, Zoomlion and others rose steadily. Future success for top Chinese construction equipment manufacturers will require sustained efforts in R&D, global distribution, and brand development to extend their competitive advantage on the world stage.